What is Consideration in GST?

Consideration includes any payment made or to be made, whether in money or otherwise, or any act or forbearance, whether or not voluntary, for the supply of goods or services, whether by the person or by any other person.

Types of Consideration

- Monetary consideration – payment by cash, cheque or credit card, bank transfer and deduction from bank account.

- Non-monetary consideration – goods or services provided as payment

Payments Not Treated as Consideration

- There is no direct link between the payment and the supply

- There is no supply of goods or services in return for the payment

- Fines and Penalty charges – unless the fine is imposed in fulfilment of terms of an agreement

- Grants

- Monetary Donation

- Sponsorship payment where sponsor does not receive any identifiable benefits in return

- Project Funding – for example, co-sponsoring a research project – funds contributed are dependent on cost of project rather than for commercial benefit

Deposit

Deposit is not part of the Consideration for the supply if it does not form part of the payment for the supply.

The following are few types of deposits:

- Forfeiture Deposit – not consideration for any supply – effectively amounts to a compensation payment for damages due to non performance of the contract or for breach of contract.

- Security Deposit – not consideration as this is merely for a security. For example, for safe return of goods on hire or loan – hence not consideration for a supply

- Return Deposit – not consideration – not part of payment but a return of money to the customer due to cancellation of the contract between the supplier and customer

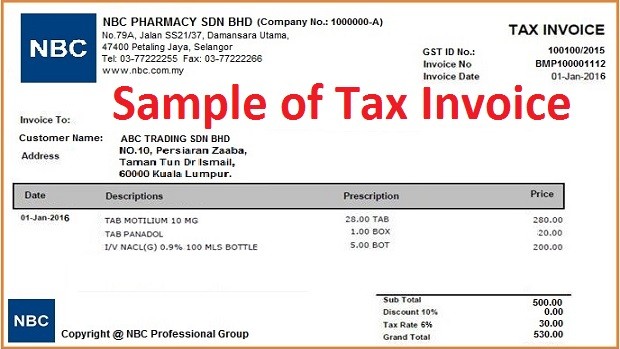

What is Tax Invoice? How to issue Tax Invoice?

What is Tax Invoice? How to issue Tax Invoice?  Basic Concepts of GST (Goods & Services Tax)

Basic Concepts of GST (Goods & Services Tax)  What is Exempt Supply in GST?

What is Exempt Supply in GST?  Scope of Goods & Services Tax (GST)

Scope of Goods & Services Tax (GST)  What is Deemed Supply in GST?

What is Deemed Supply in GST?  What is 21 Days Rule in GST? (Time Bomb in GST)

What is 21 Days Rule in GST? (Time Bomb in GST)  What is Blocked Input Tax Credit in GST?

What is Blocked Input Tax Credit in GST?  What is NOT a Supply in GST?

What is NOT a Supply in GST?